Questions continue to be raised regarding the viability of a proposed coal mine involving the Kalpowar Land Trust, Aust-Pac Capital Pty Ltd and new joint venture participant Bounty Mining.

The profile of yet another Queensland coal mining project is likely to increase as the small, specialist mining company Bounty Mining has made a deal which may see it taking a controlling 51% share in the risky development proposal, leaving Indigenous Traditional Owners with a mere 12.5% stake. Publicly listed Bounty Mining Ltd (ASX share market code: BNT) now plan capital-raising to fund “…feasibility studies and finalisation of the Environmental Impact Statement [EIS].”

Environmental threats and economic risks.

Is this the future for Cape York?

Environmental approvals seem far from certain noting that:

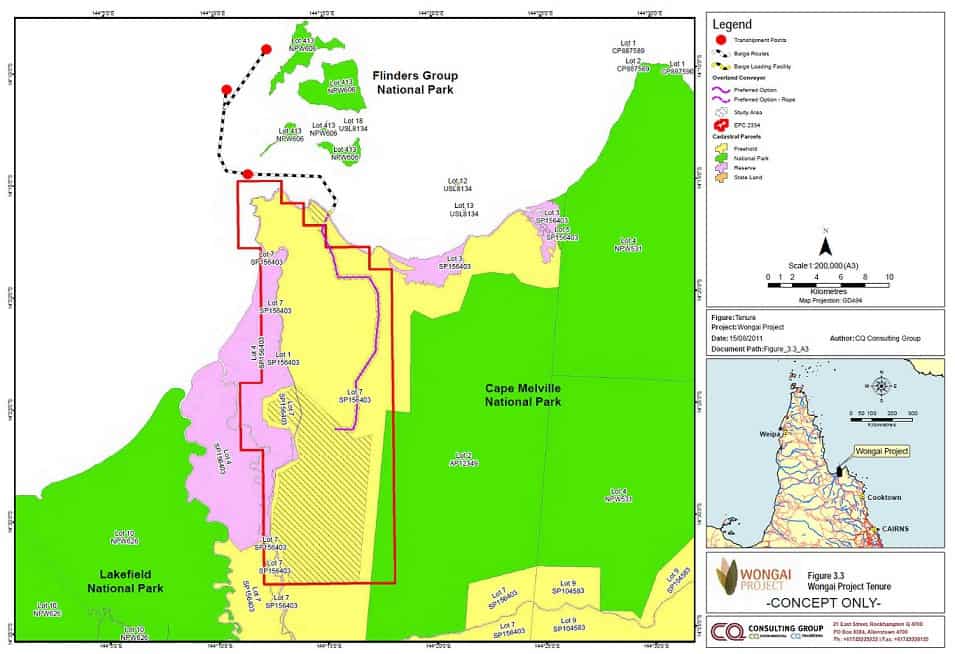

- The mine site is adjacent to the Lakefield and Cape Melville National Parks and the Great Barrier Reef Marine Park and contains a nature reserve. The Wongai coal mine is proposed for the shores of Princess Charlotte Bay on Cape York (about 150 kilometres northwest of Cooktown)

- The proposal involves coal transhipment points, adjacent to the Flinders Islands in the waters of the Great Barrier Reef World Heritage Area. The proposal would introduce barges, three coal transhipment points and additional shipping to an area currently free of such activities.

- There are significant wetlands on and adjacent to the property that could easily be damaged by any underground activities disturbing the aquifers of the region. The depth of the mine and bord and pillar mining method is likely to cause subsidence issues.

- The proposal features a haul road through wildlife rich country.

Mutiny on the Bounty?

It is interesting to note that in the Bounty Mining preliminary final report for the year ending June 2013 (available as an ASX announcement) the company states “In June 2013 Bounty announced a programme of redundancies to align operations with reduced demand for coal mining services in the current economic climate” and “VETL Pty Ltd (VETL), a company associated with Bounty’s chairman is the main lender to Bounty. On 1st August 2013 the independent directors determined that Bounty does not have the means to make further loan repayments to VETL.”

Will Bounty Mining be able to raise the funds from share sales or loans to turn an environmentally risky, socially questionable and economically doubtful mine into a reality?

Even if the mine goes ahead how many of the speculated 200 odd jobs would go to locals? One wonders if along with the inevitable damage to environmental values and risks to the important cultural values of the area, could the Traditional Owners be left with only 12.5% of an unprofitable mine? Do they actually risk being worse off (liable) if the mine goes under -left with a damaged landscape and no funding for rehabilitation?

Links:

Background: Wongai – FNQ’s Franklin River? March 20, 2013 By Brynn Mathews

Bounty Mining: http://www.bounty.com.au/

Aust-Pac Capital: http://www.wongaiproject.com.au/

Media article: ‘Threat to Barrier Reef raised as indigenous mine deal signed’, The Australian newspaper, Sept 16:

You can find out more about this project and the status of the referral and assessment process under the EPBC Act by clicking here.